Unless you love numbers, creating an income statement for your business might seem like a tedious challenge. Especially in the face of everything else you need to do to keep the boat afloat!

But this simple task could save you an enormous amount of time and money.

To make things easier, here’s a rundown of everything you need to know about income statements, along with step-by-step instructions and templates to help you create your first one.

How to create an income statement

The purpose of an income statement is to see if your business is making money or losing it. It also comes in handy when applying for a loan or courting investors. Here’s how to create one.

- Pick a reporting period.

- Produce a trial balance report.

- Add up what you earned in that period.

- Determine how much it cost you to produce your goods/service.

- Calculate your margin.

- Tally your operating expenses.

- Now calculate your income.

- Don’t forget taxes.

- Figure your net income.

- Formalise your income statement.

Before we dive into the steps, let’s quickly explain why this statement is useful for even small businesses. When you’re ready to start punching in numbers, use one of these 5 income statement templates. We even provide templates for restaurants and year-on-year reporting.

What is an income statement?

An income statement, also called a profit and loss statement, is a report that shows the revenue, expenses and net income or loss for a period.

An income statement shows you whether you’re making money or losing it.

Before you create your first income statement, you should know that there may be some circumstances where a specific income statement format is required.

For instance, if you’re applying for a loan the bank may wish for you to format your income statement in a particular way. Be sure to ask about this before organising, recording or submitting your information.

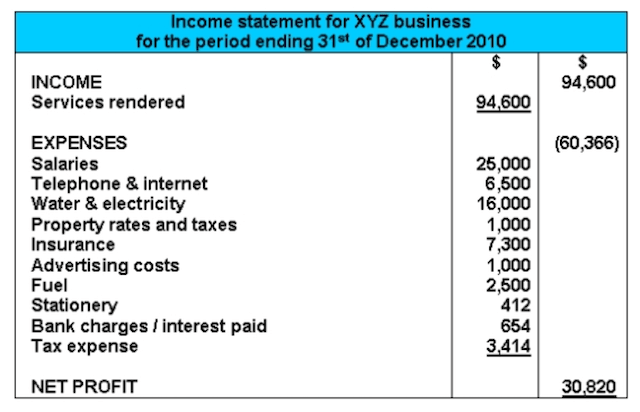

Source: Accounting Basics for Students.

To create an all-purpose income statement and report the profits your small business is generating, follow these 10 simple steps:

1. Pick a reporting period

Before you start to gather the numbers needed to prepare your first income statement, you will need to choose the reporting period your report will cover. To determine your reporting period, check out the information in “How often should you create an income statement?” below.

2. Produce a trial balance report

Now you’ll need to print out a standard trial balance report.

Trial balance reports list the end balance of each account in the general ledger for a specific reporting period. This will give you most of the figures you need to create an income statement.

You can easily generate a trial balance through any cloud-based accounting software or by hand here.

3. Add up what you earned in that period

Next, you’ll need to tally up your business’s total sales revenue for the reporting period.

Revenue includes all money earned during the reporting period, even if you haven’t yet received payment.

Add up all the revenue line items from your trial balance report and enter the total amount in the revenue line of your income statement.

4. Determine how much it cost you to produce your goods/services

The cost of goods or services sold (COGS) includes everything you’ve spent in order to provide your goods or services during the reporting period. This could include:

- Direct labour

- Materials

- Shipping

Add up all the COGS line items on your trial balance report and list the total on the income statement, directly below the revenue line item.

5. Calculate your margin

Next you’ll want to subtract the cost of goods sold total from the revenue total on your income statement.

This calculation will give you the gross margin or gross amount earned from the sale of your goods and services.

6. Tally your operating expenses

Add up all the operating expenses listed on your trial balance report. These are all the costs of running your business that are not directly associated with production.

Enter the total amount into the income statement as the selling and administrative expenses line item. It’s located directly below the gross margin line.

7. Now calculate your income

Subtract the selling and administrative expenses total from the gross margin. This will give you the pre-tax income. Record the figure at the bottom of the income statement.

8. Don’t forget taxes

To calculate income tax, multiply your applicable tax rate by your pre-tax income figure. Add this to the income statement, below the pre-tax income amount. You’ll find handy tax calculators here.

9. Figure your net income

To determine your business’s net income, subtract the income tax from the pre-tax income figure. Enter this amount into the final line item of your income statement.

Note that if your revenues are greater than expenses for the reporting period, you have net income. If revenues are less than expenses, you have a net loss.

10. Formalise your income statement

To finalise your income statement, add a header to the report identifying it as an income statement, along with your business details and the reporting period covered by the income statement.

What’s an income statement used for?

Creating an income statement can help you make decisions regarding spending and investing. By looking at your income statement, together with your cash flow statement and balance sheet, you’ll gain insight into how well your business is doing financially.

Income statements show you how much you’ve spent on various expenses, giving you a comprehensive overview of your business’s financial strengths and shortcomings. You can use this information to decide if it’s time to invest in that new piece of equipment or if it would be better to wait.

Potential investors interested in your business will also want to see an income statement.

By providing this key financial record, you’ll be able to demonstrate how your net income is calculated over different fiscal periods. This information will help investors understand potential for growth in your business.

Having this core data available will also establish you as an organised, competent and experienced entrepreneur.

How often should you create an income statement?

Businesses typically report their income on one or more of these frequencies:

- Yearly

- Quarterly

- Monthly

Publicly-traded companies are required to prepare financial statements on a quarterly and annual basis, but small businesses aren’t as heavily regulated in their reporting.

But creating monthly income statements can help you identify trends in your business, revealing how profits and expenditures ebb and flow over time. You can then use this insight to make strategic decisions that improve efficiency and keep you from coming up short during dry spells.

Get a jump-start with these income statement templates

The quickest way to create an income statement is to use one of these templates:

Microsoft Excel income statement template

Microsoft Word income statement template

Income statement template for a restaurant

Income statement template for a small business

Income statement template year-on-year comparison

See — that wasn’t that hard!

Once you start creating income statements for your business on a yearly, quarterly or even monthly basis, you’ll see financial reporting is a smart way to keep your business on track fiscally.

In just 10 simple steps, you will have all the information you need to gauge the financial health of your business!

The above content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.