As a senior bookkeeper with over 23 years of experience, I have seen it all — from business owners raking in the cash to losing their homes due to careless bookkeeping. Sure, it’s great when you are making the money, but you cannot grasp the state of your business financials by their bank balance alone. The only way to gain the knowledge needed is to use all the accounting reports, including the trial balance.

If you are doing your bookkeeping by hand, you’ll want to create a trial balance on a regular basis.

Knowing your numbers so you can grow your numbers is extremely important to long-term success.

Related: Save money with these small business accounting tricks

Create a trial balance in 5 steps

For anyone managing their business finances by hand, a trial balance can be a lifesaver when things don’t add up. Here’s how to create one:

- Set up your statement.

- Add the accounts from your balance sheet

- Add the accounts from your income statements.

- Enter the figures into your statement.

- See if the columns match.

Before I walk you through the steps, I’d like to briefly explain what this calculation does for a small business. Looking for an example of a trial balance sheet? Scroll down.

What is a trial balance?

A trial balance is a list of all the accounts that are in the ledger of the bookkeeping file for a business. It is the only accounting report that lists all capital and revenue accounts. This means it is the only report that shows the accounts from both the balance sheet and income statement.

A trial balance helps you find any errors in double-entry accounting.

Now, don’t let the term ‘double-entry accounting’ scare you because it simply means that the accounting system uses debits and credits to create the financial statements.

The debits and credits need to be equal (to ‘balance’) for the financial statement to be correct. If the total of each column does not match (balance) then there is an error in the reporting.

With all the different accounts in a bookkeeping system, it is very easy to make mistakes. These mistakes then become errors in the financials, which cause the profit in a business to be over- or understated.

Common errors revealed

Using the trial balance in your business will help you to discover the following:

Posting mistakes

If you are posting transactions using general journal entries, your debits and credits might not balance, especially if you are manually recording your transactions.

Transcription errors

Sometimes a business owner can transpose numbers when posting the dollar amounts. For example, entering $435 instead of the correct amount of $453. The trial balance will find these errors for you.

Accountant transitions

When an accountant is working on the year-end, they will pull the information needed from the file that is provided to them. They use the trial balance to confirm that they transferred the information correctly.

Calculation errors

If the debit and credit columns don’t match, chances are the addition of each column may be calculated incorrectly.

There are some exceptions though. A trial balance will not show you:

- The transactions that you missed or did not enter into the system

- If the debit and credit were incorrectly swapped in a transaction (because this error cancels each side of the transaction out)

Make sure you are entering all the figures correctly and in the right column for every transaction.

How to prepare a trial balance

Because we are living in the 21st century, there is accounting software that automatically creates the trial balance for you. As you enter the transactions, the software takes every transaction and places it on your trial balance automatically.

Accounting software takes the time, energy and headaches out of doing this by hand.

But if you are manually posting your bookkeeping transactions into a paper book or into software like Excel or Google Sheets, then it is vital that you know how to create a trial balance. This is the only way to make sure your bookkeeping records balance.

Let’s create a trial balance for your business

You will need to gather all your transactions for the time period you are working on. The start date for your transactions should be the first day of your fiscal year and the end date would be the date you are working up to. This date can be any date between the first day and the last day of your fiscal year.

1. Set up your statement

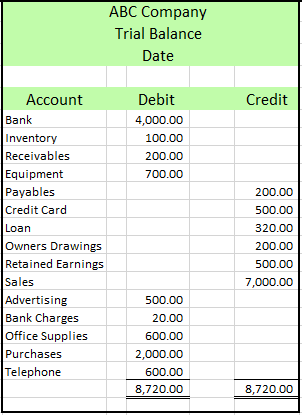

You will need three columns: account, debit and credit (in this order, from left to right). You can use a trial balance template to get started quickly.

2. Add the accounts from your balance sheet

Next you need to add the accounts from your balance sheet:

- Assets (bank, accounts receivable, inventory, furniture and equipment accounts)

- Liabilities (all debts, credit cards, accounts payable, loan accounts)

- Equity (owner’s drawings, retained earnings)

3. Add the accounts from your income statements

This includes revenue (all sales accounts) and expenses (all expense accounts).

4. Enter the figures into your statement

Add the dollar value for every account under the correct debit or credit column (this comes from the data you collected).

5. See if the columns match

Total the debit column and then the credit columns separately.

If your debit column matches your credit column, then your bookkeeping balances. If they do not match, you will need to check your math and make sure the debits and credits are in the correct columns.

With a completed trial balance, you can verify that the accounts and dollar values on your balance sheet and income statements are accurate. You can also pass the trial balance on to your accountant to help them verify your year-end numbers. The information on the trial balance can also help you create other reports like a budget and a cash flow statement.

Accounting is your friend

As a partner in a bookkeeping and business consulting firm, trust me when I say that accurate recordkeeping is extremely important to the health of any business, no matter how small. Not to mention that it helps when dealing with the government. For anyone managing their business finances by hand, the trial balance is a vital way to find errors and set them right.