When you run a small business, you need to know how to gauge your business’ financial health. One of the most important financial documents for any business, no matter how small, is an income statement (aka profit and loss statement).

Why you need an income statement

An income statement produces a snapshot in time of your business’s activities, including whether it’s earning a profit or taking a loss.

It takes information such as revenue, expenses, cost of goods for resale and taxes paid to show you the net profit of your business.

With an income statement, you can tell how your business is doing at a glance. This helps you make the right decisions about:

- Business spending

- When and how much to invest

- Whether or not you need to make a change

Comparing several years of these documents will improve your ability to make projections and strategize your future goals.

You should generate an income statement at least annually. To keep a closer eye on business performance, you could benefit from monthly income statements.

Create your first income statement in 3 steps

The quickest way to get a sense of your financial health is to:

- Add up your business revenue.

- Calculate your total expenses.

- Subtract your expenses from total revenues.

For those who need a more in-depth view, try the multi-step income statement described below.

How to create an income statement

There are two types of income statement: single-step and multi-step. A single-step statement simply subtracts your total expenses from your revenue to show your net income. In other words:

Net Profit = Revenues - Expenses

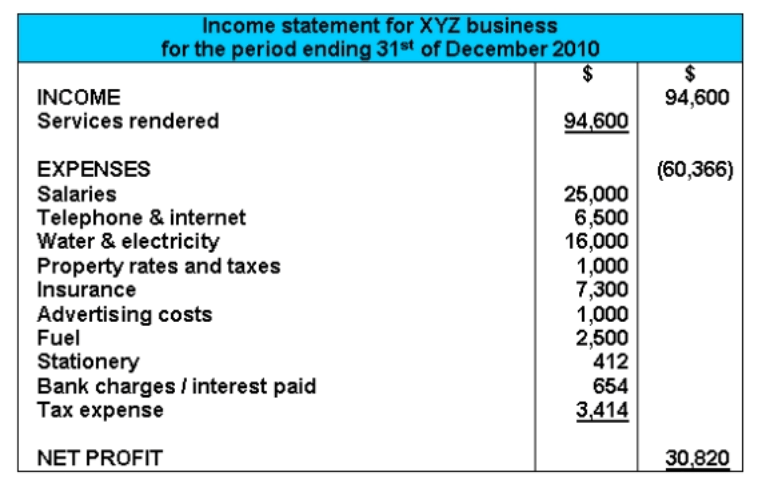

You can find a single-step income statement example below:

Source: Accounting Basics for Students.

This is an excellent model for businesses that provide a service and do not need to calculate the cost of goods sold.

1. Add up your business revenue

Revenue includes your operating revenue, non-operating income and gains.

Operating revenue

This includes money earned through the primary activities of your business. For example, retailers, wholesalers and manufacturers would get their operating revenue from the sale of goods. Service providers like lawyers, photographers, graphic designers, dog walkers, etc. earn money from the services they provide.

Non-operating revenue

This is recurring income earned through non-core activities. For example, non-operating revenues might include:

- Earned interest

- Rental income

- Royalty payments

- Income from another business’s advertising

Examples might include the money a restaurant receives for advertising space on their outside wall, or a company receiving rent checks for subleasing office space they are not using.

Gains

Sometimes called “other income,” gains are non-recurring revenues earned from activities such as the sale of equipment or long-term capital assets. For example:

- An old vehicle

- Unused property

- A subsidiary or entire business

Taken together, these categories constitute business revenue, or income.

2. Calculate your total expenses

Your expenses are the costs that go into producing and selling goods and services, as well as non-operating expenses and non-recurring losses.

Operating expenses

Expenses related directly to your primary business activities include:

- Payroll

- Rent

- Insurance

- Utilities

- Technology costs

- Marketing

Non-operating expenses

Expenses not related to your core business activities. The most common example of this would be interest on debt payments.

Losses

Losses from non-recurring events such as the sale of a capital asset (e.g. buildings, equipment or stocks).

Cost of goods sold

The costs that go into creating goods, including:

- Raw materials

- Labor costs

- Warehousing

- Packaging

Costs such as sales and distribution are not included and should be part of your operating expenses.

Calculating your expenses on an income statement can help you see what you’re spending money on, where you might be overspending and how you can get back to profitability.

Related: Save money with these small business accounting tricks

3. Subtract your expenses from total revenues

The answer gives you a quick idea of whether your business is financially healthy or not.

For a more detailed look at your financial health, there’s a second income statement option.

Option #2: The multi-step income statement

A multi-step statement breaks down the difference between operating and non-operating revenue and expenses. It also shows a third expense category: cost of goods sold.

This is especially useful for retailers, wholesalers and manufacturers.

This type of statement will give you a more detailed picture of your business finances including revenue, expenses, gains and losses.

Cost of goods sold

The cost of goods sold includes all of the expenses that go into acquiring or producing goods.

- For a retailer, it would be what you paid your wholesaler or supplier.

- For a manufacturer, the cost of goods sold would include raw materials and machinery costs.

Gross profit

Your gross profit (aka gross margin) is your net sales minus the cost of goods sold. This will show you how much you make after subtracting the cost of products you manufacture or resell, but not other operating expenses like payroll or rent.

It can help identify whether unprofitability is the result of:

- High cost of goods sold

- Low net sales

- High overhead expenses

This tells you where to focus to make your business profitable.

Operating income

The formula for operating income is:

Operating income = Gross Profit – Total Operating Expenses

If you notice a large gross profit margin disappearing at this stage, you could have a problem with operating expenses.

Net income

Finally, your net income determines how much money is left in the business after all expenses, including taxes.

Because businesses are taxed based on their net profit, your net income shows how much is available to be reinvested or drawn out as dividends once taxes have been paid.

Cash method vs. accrual method

Small business owners often ask when they should record revenue. That depends on the accounting method you use — the cash method or accrual method.

Cash method

With the cash method, you wait until you receive or send payment to record the transaction on your income statement. This means you would recognize a sale or payment in the month that money changes hands.

One tool you can use to separate received money from money you do not yet have in hand is listing this income as “Accounts Receivable.” Likewise, expenses are recorded when they are incurred, not when they are paid.

Accrual method

With this method, you record revenue on your income statement when you earn it — in other words, when you provide the goods or services for which you charge. You do not have to receive the payment to record it.

Take charge of your business finances

If you’ve never created a financial statement before, start with one of the income statement templates available online. A snapshot like this can help you see:

- Where you’re succeeding

- Where you can improve

- How you can invest business funds more productively in the future

You can create an income statement annually or monthly, choosing a simple, single-step statement or a more detailed multi-step statement for a closer look at your business.