Running a business can be pretty stressful. In fact, 45% of small business owners report feeling stressed and anxious by the daily toll that entrepreneurship can impart. Monetary concerns are a big part of this overall stress, so solving a portion of this common stressor early is key if you’re a small business owner or an aspiring entrepreneur.

Credit card processing is a routine part of business, and finding a solid processing provider should be a smooth process, not a source of stress. In this guide, we’ll cover the basics of credit card processing, the costs involved, and how to choose a credit card processor that works for you.

Let’s go.

Level up your payment processing with GoDaddy Payments.

What is credit card processing?

Credit card processing enables the flow of funds from the customer's bank to the merchant's account and includes authorization, batching, clearing, and funding steps. Payment processors handle the technical aspects of moving money between customers and merchants on behalf of the merchants.

To break that down a bit, when a customer pays with a credit card, the merchant sends the transaction details to the credit card network. The network checks with the customer's bank to make sure the card is valid and has enough funds. If approved, the bank puts a hold on the funds in the customer's account.

At the end of the business day, the merchant bundles all transactions and sends them to their payment processor. The processor facilitates transferring the funds from the customers' banks to the merchant's bank account, which usually takes 1-3 business days.

So, in short, credit card payment processing involves the merchant, credit card networks, banks, and payment processors working together to move money from the customer's account to the merchant's account.

Who is involved in credit card processing — key components

Credit card processing has many moving parts; here’s a quick breakdown of each:

- Cardholder: The customer purchasing goods or services with their credit card. They initiate the transaction.

- Merchant: The business accepting credit card payments. They need payment processing services to accept cards.

- Payment gateway: The intermediary between the merchant and processor that facilitates authorizing card transactions.

- Payment processor: The company that handles transferring funds from the issuing bank to the acquiring bank.

- Card network: The credit card company (Visa, Mastercard, etc). They set the rules and standards for processing.

- Issuing bank: The bank that issued the credit card to the cardholder. They authorize transactions.

- Acquiring bank: The bank that handles deposits for the merchant. They facilitate transferring funds into the merchant's account.

- POS system: The point-of-sale (POS) system that integrates with payment gateways and processors to accept and record card transactions.

Related: Learn more about POS systems

How credit card processing works

Let’s take a closer look at what happens during the transaction process:

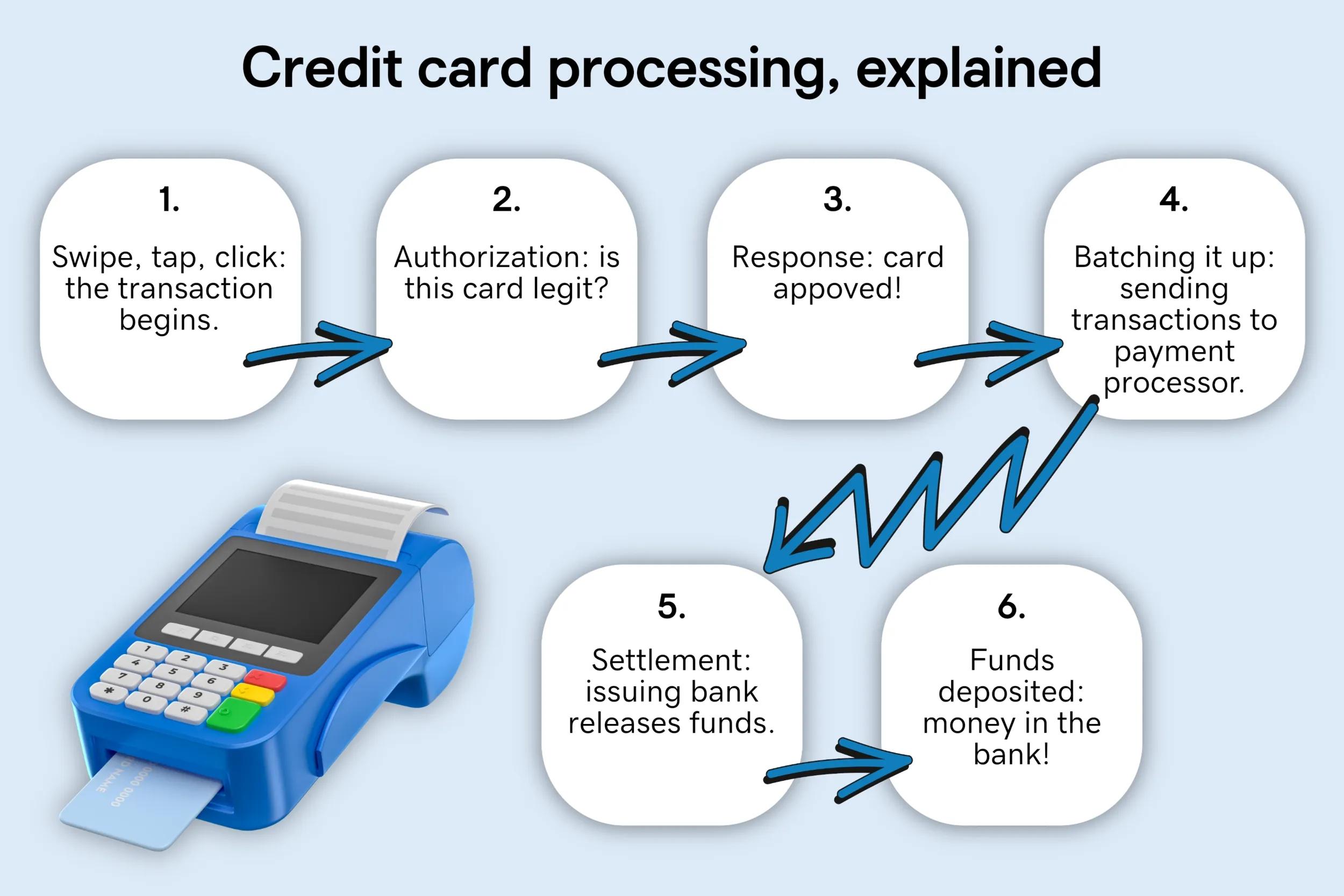

- Purchase: It all begins when a customer pays with their credit card, either by swiping their card at a terminal, tapping their contactless card, or entering their card information online. This sends the credit card details to the merchant's system.

- Authorization: The merchant's payment gateway sends the credit card data to the card network (Visa, Mastercard, etc). They verify with the issuing bank that the card is valid and the customer has sufficient funds or credit.

- Response: If everything checks out, the issuing bank sends back an authorization code. This reserves the funds on the customer's credit limit, but doesn't charge their account yet.

- Batch closure: Throughout the day, the merchant's point-of-sale system stores authorized transactions. At the end of the day, they "batch" all the transactions and send them to their payment processor.

- Clearing/Settlement: The processor forwards the batch to the card network, which tells the issuing bank to release the funds. The acquiring bank then deposits the funds into the merchant's account minus any processing fees.

- Funds deposit: In one to three business days, the funds clear, and the merchant has access to their money. The customer's account is finally charged for the transaction. Transaction complete!

What are the benefits of credit card processing?

Accepting credit card payments is a must for businesses these days. Here’s a few benefits of credit card processing for business owners:

- Improved customer experience: With merchant credit card processing, businesses can accept a range of payment methods, allowing customers to easily pay using their preferred method.

- Fewer missed sales opportunities: Most customers prefer to pay with plastic rather than cash, so merchants who don't accept credit cards tend to lose business to competitors who do.

- Increased flexibility: Credit cards allow buyers to make purchases online or over the phone, so merchants have increased flexibility on where they're able to make sales.

- Quicker access to funds: Merchant credit card processing also provides quick access to funds, enabling merchants to get paid within 1-3 business days. This improved cash flow helps operations run smoothly.

- Enhanced security: Accepting credit card payments is more secure than dealing with paper checks or cash.

How much does credit card processing cost?

Credit card processing fees are paid by the merchant when accepting credit card payments and generally range from 1.5% to 3.5% of the transaction total. There are other factors to include in the overall cost of credit card processing, like which company you’ve chosen as your payment processor, the type of credit card used, and how that card is processed.

Credit card processing fees are made up of three parts: interchange fees, assessment fees, and payment processing fees.

- Interchange fees: Fees charged by the credit card networks (Visa, Mastercard, etc) to process transactions. It covers the issuing bank's risk. Rate is typically a percentage of the transaction value and a small fee per transaction.

- Assessment fees: Charged by the card network to fund their operations. Generally a small flat fee per transaction.

- Payment processor fees: Charged by the payment processor to facilitate moving funds from issuing to acquiring bank. Can be a percentage or flat fee per transaction.

Choosing a credit card processing provider

Your credit card processor is an important part of your business, so it’s vital that you carefully consider the processor you ultimately work with. When weighing your options, these are the factors that you’ll want to include in your search:

- Pricing: Compare rates and fees across providers. Beware of hidden fees.

- Features: Evaluate integrations, reporting, inventory management, etc. Ensure the provider offers everything you need.

- Customer support: Look for responsive customer service and extensive resources/documentation. Downtime costs you money.

- Security: The provider should be PCI compliant and offer fraud protection tools. Make sure your data is secure.

- Contract terms: Check contract length, early termination fees, and billing practices. Avoid long or auto-renew contracts.

- Payment methods: Evaluate what types of payments are supported (credit cards, mobile wallets, etc).

Check out this list of best credit card processing companies for an expanded list of payment processors.

Credit card processing best practices

As a business owner, there are some best practices to consider when maintaining your business payment processing. Here are some of the key steps to keeping your business on track:

- Review statements regularly: Scrutinize statements every month to identify any incorrect charges or fees. Dispute them promptly.

- Understand your fees: Know what you are being charged for interchange, assessments, processing, etc. Ask your processor to explain any unclear fees.

- Maintain PCI compliance: Follow PCI data security standards to keep customer card data safe and avoid non-compliance fees.

- Offer online payments: Let customers pay invoices or make purchases online via payment gateway integration.

- Train staff properly: Ensure staff knows proper card processing procedures to avoid costly mistakes.

- Compare providers periodically: Re-evaluate different processors occasionally to get the best rates and features.

- Have a backup plan: Have a contingency, like a backup terminal, in case your equipment fails to avoid disrupted sales.

- Maintain clear and consistent refund policies: Providing clear policies is good for customer service and can help to reduce the possibility of chargebacks.

Conclusion

Accepting credit and debit card payments is essential for businesses. The key to getting the most out of your credit card processing is to understand the fee structure, choose a reputable provider, utilize security features, follow best practices, and monitor statements regularly. Comparing providers periodically can also ensure you are getting competitive rates.

Level up your payment processing with GoDaddy Payments.

With the right credit card processing solution and habits, businesses can streamline payment collection, reduce headaches, and provide the flexible options that today's customers expect. Though processing fees are unavoidable, they allow you to tap into the many benefits of accepting credit and debit cards.