As I have moved along in my career, I have come to realize that a vast majority of business owners who have employees want to do what is right by them. They want to pay the people who work for them a fair wage, and provide a good benefits package. Part of that benefits package is a pension or profit sharing plan. So, can you deduct contributions to pension and profit sharing plans?

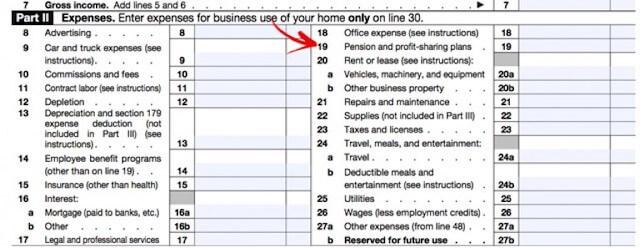

Yes! The contributions you make on behalf of your employees, as well as the fees you pay for a pension or profit sharing plan, are deductible. You include these expenses on line 19 of the Schedule C.

Disclaimer: This content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

Types of pension and profit sharing plans

Pension and profit sharing plans are not as familiar to most people as are the costs of things like office supplies. There are different types of plans available to small businesses, including:

A Self Employed Pension (or SEP) plan, which allows business owners a relatively simple method to contribute towards their employees’ (as well as their own) retirement plans. You make contributions to an Individual Retirement Account or an Annuity that is set up for each person participating in the plan. The IRA is a traditional IRA, which needs to follow the same investment, distribution and rules as an IRA outside of the SEP.

A Savings Incentive Match Plan for Employees (SIMPLE) is a retirement plan that allows both employees and employers to contribute to a traditional IRA. These types of plans are designed for small businesses that are not sponsoring a retirement plan.

A 401(k) plan, according to the IRS, is “a qualified (i.e. meets the standards set forth in the Internal Revenue Code (IRC) for tax-favored status) profit-sharing, stock bonus, pre-ERISA money purchase pension, or a rural cooperative plan under which an employee can elect to have the employer contribute a portion of the employee’s cash wages to the plan on a pre-tax basis.” The big difference between a 401(k) plan and the other types of retirement plans is that the 401(k) plan requires a lot more paperwork.

How to deduct contributions to pension and profit sharing plans

Unlike most of the other lines on the Schedule C, you will need to fill out additional forms if you deduct pension and profit sharing costs.

If you have a one-participant plan that only covers you or you and your spouse, or only you and one or more of your partners (or your partners and their spouses), you can complete form 5500-EZ, “Annual Return of One-Participant (Owners and Their Spouses) Retirement Plan.”

If you have a plan with fewer than 100 participants, and are exempt from the requirement that the plan’s books and records be audited by an independent qualified public accountant (the IRS can let you know this), you may be able to use form 5500-SF, “Short Form Annual Return/Report of Small Employee Benefit Plan.” Otherwise you need to complete form 5500, “Annual Return/Report of Employee Benefit Plan.”

You should receive a statement from your plan provider telling you the amount you contributed to a pension, profit sharing, or annuity plan, or plan for the benefit of your employees.

If the plan included contributions made for you, enter those contributions made as an employer on your behalf on Form 1040, line 28, or Form 1040NR, line 28, but not on line 19 of your Schedule C.

So what happens if you decide just to fill in the amount on line 19, but don’t file the appropriate 5500 form? The IRS will penalize you $25 a day, with a maximum penalty of $15,000 (that works out to 600 days of not filing), for not filing those forms with your tax return. Avoid that.